CONFLICT IN STRATEGY PART 3: THE CONFLICT MAP

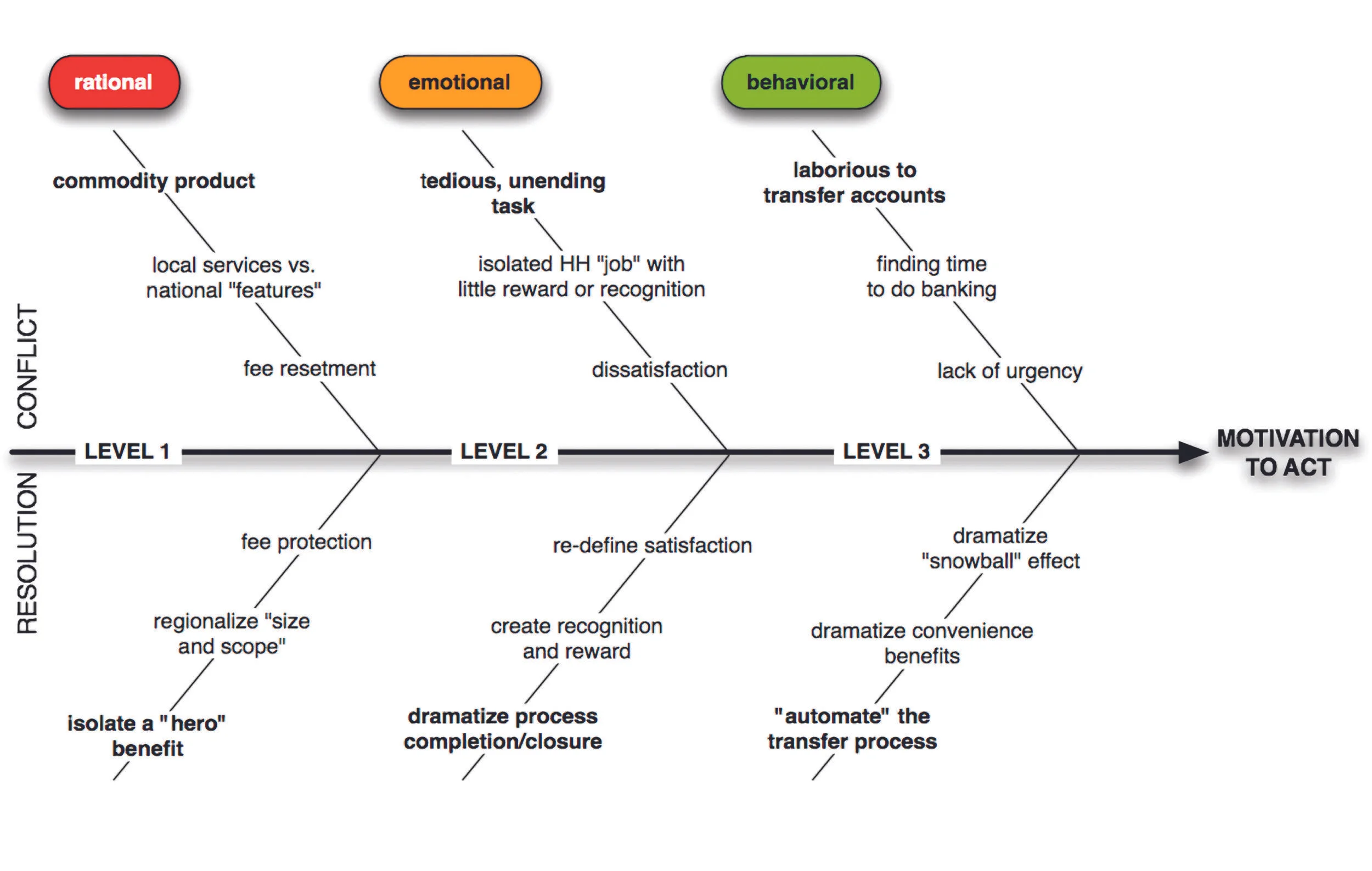

Here’s an example of a Conflict Map in action for a new free checking account offering from a bank. Target is young families (adults 24-39). Here are the conflict and resolution “bones” on the Conflict Map:

CL1: RATIONAL

Primary Conflict – commodity product – consumer perceives checking accounts in general, and “free” checking accounts in particular, to have few if any real points of difference. As an extension, “free” becomes code for hidden fees, which creates cynicism.

Primary Resolution – isolate a “hero” benefit – the antidote to commodity is to brand the strongest feature/benefit and isolate it in the communications. Thus, “free checking” becomes a subordinate reason to believe, not the headline.

Sub 1 Conflict – local service vs. national “features” – consumer is torn between being true to his/her community and the trust a local establishment offers vs. the access features and new technology offered by larger banks.

Sub 1 Resolution – regionalize size and scope – a middle ground between super-bank and local player may bridge gap between desire for trust and desire for access features that are distinguishing.

Sub 2 Conflict – fee resentment – a fairly uniform and pervasive undercurrent of resentment exists over being charged fees for access to one’s own money regardless of the costs/business imperatives of the bank.

Sub 2 Resolution – fee protection – leverage the tried-and-true guarantee, which can be positioned in the form of “we’ll always be up front with you,” or “no hidden fees, guaranteed,” depending on the degree of acceptable liability.

CL2: EMOTIONAL

Primary Conflict – tedious, unending task – because family finance is a continuous process, there is little closure for the hard work incurred each month. Consumer links the checking account to negative attributes: “cash out vs. cash in,” and tedious bookkeeping.

Primary Resolution – dramatize completion/closure – demonstrating the satisfaction of finishing or producing vehicles to dramatize/manage the results of maintaining a checkbook will help provide sense of accomplishment.

Sub 1 Conflict – isolated HH (household) “job” w/little reward of recognition – considered more an errand or chore rather than financial stewardship, and usually relegated to a single person, there is little emotional payoff, hence product “loyalty.”

Sub 1 Resolution – recognize the person in the household responsible for managing the checking account and/or give them “rewards”; elevate their status in the household.

Sub 2 Conflict – dissatisfaction – consumer may have had a service conflict or may be dissatisfied simply because there is no element of the experience that is particularly satisfying.

Sub 2 Resolution – re-define satisfaction – define for the consumer what it means to be satisfied by their banking relationship, then deliver heavily on that promise.

CL3: BEHAVIORAL

Primary Conflict – laborious to transfer accounts (direct deposit, etc.) – significant inertia and “fear” (of potential complications) associated with physically moving existing relationship from one bank to another.

Primary Resolution – provide process shortcuts – offer services and tools that “automate” the burden and risk of moving accounts (notably, ensuring sufficient balances in the old account as final checks clear; ensuring smooth transfer of direct deposit; completing necessary paperwork).

Sub 1 Conflict – finding time to do banking – ability of consumer to visit branch due to time restraints, distance, etc. limit motivation to act quickly.

Sub 1 Resolution – aside from extended banking hours, provide promotional time periods in which the bank is open – late evenings, Sundays, tabling at community events, etc. – for acquisition drive periods; create automated tools/reminder in concert with online banking.

Sub 2 Conflict – lack of urgency – in the scheme of the other conflicts the consumer is dealing with, dissatisfaction with his/her bank or the appeal of a promotional offer are low, precisely because their existing checks are still “working” just fine. It’s only when there is a defining dissatisfaction moment or the consumer moves that changing banks is truly top of mind.

Sub 2 Resolution – dramatize the “snowball” effect – remind the consumer that the longer they stay where they “don’t want to be,” the harder it is to move when they want to. Additionally, appeal to the consumer’s desire for change in ways that seem truly aspirational vs. laborious.

Reviewing the Conflict Map for free checking underscores why those banks that have become more retail oriented appear to be out-performing those that continue along the more traditional path. Early in the game, free checking was a compelling point of difference. Today, it is a commodity offering. So though a consumer may be enticed by a $50 gift card, it is not enough to blast past the first conflict of commodity.

The retail model of these brands emphasizes extended hours (time conflict), a less institutional branch environment (commodity conflict), rewards for routine transactions (job with no reward conflict), community “fun” (national features vs. local trust conflict), and no-fee ATMs outside of network (fee resentment conflict). The creative strategy of this retail orientation is evident in their communications – everything from the branch merchandising, to the brand advertising, direct mail and promotional campaigns.

What few, if any banks, have truly mastered at the point of this writing are tools that “automate” the process of switching accounts. A bank with a retail bias that can crack this code is sure to succeed. It’s important to note that the structure of the map and the number of influencing- conflicts differs from marketing challenge to marketing challenge. You have to sort out everything you know ... break it down! A logical construction will inevitably emerge.

For now, the big takeaway is that recognizing consumer conflicts is the strategic underpinning of any marketing campaign or project that you embark on. Creative strategy is built on consumer insight – it’s what drives your critical decisions involving:

What component(s) of the value proposition to key in on

How to make that key component of the value proposition more relevant

Primary and secondary decisions hurdles that should inform your CRM/eCRM and retargeting cadences

Add depth/nuance to your personas for more actionable audience development

Reprinted from Deconstructing Creative Strategyby Rich Feldman, all rights reserved. For a free copy email richfeldman@landtheplane.net